If you’re a small business owner in need of some quick cash, you may have come across Kabbage Funding. Or, if you’re like me, you have received countless Kabbage invitations in the mail.

You may even be exploring starting a business of your own. After all, this past year has taught us that it’s never too late to pivot and take a shot at being your own boss.

In fact, 63% of small business owners are over 40 years old.

However, the next generation of entrepreneurs is getting in on the business game too.

Millennials and GenZs are 188% more likely to start their own business.

But every business owner will, at some point, need to make an important decision: how to finance and manage cash flow for their business.

This article will break down Kabbage Funding by American Express and three alternative small business financing and banking options.

Kabbage leads the pack of a new breed of online lending platforms helping small businesses secure quick loans at convenient terms. Small business owners who cannot fulfill the requirements of traditional lenders can easily access a line of credit on Kabbage.

With Kabbage, businesses can enjoy ample funding flexibility, raising funds whenever the need arises. The loans range from $2,000 to $250,000 and can be used to fund e-commerce inventory, payroll, operational costs, or marketing and advertising campaigns.

What’s more, you can raise funds as often as you want without ever worrying about expenses like application or origination fees, maintenance fees, or payment penalties.

This guide is designed to help you determine if Kabbage is the right fit for your business funding needs. We’ll look at how the platform works, some of its important terms and conditions, and how to apply for a quick loan.

Kabbage also has some drawbacks, which some competitors are vying to capitalize on. If you have some reservations about Kabbage, we’ll also be looking into the offerings of some of the most popular competitors in the space.

Kabbage from American Express

Overview

Kabbage is a small-business banking subsidiary of American Express Co. It was founded in 2008 as a small business bank and then upgraded to a lending platform two years later in 2011.

Today, fair-credit borrowers can secure access to cash of up to $250,000 on the platform. As a fair credit loan facility, you can qualify with a credit score as low as 640, which falls in the fair range of FICO scores.

While the platform sets aside most requirements of traditional lenders, it does require a personal guarantee. Business owners must take personal responsibility for their business loans.

Let’s take a closer look at some of Kabbage’s most notable offerings

Key Features

The platform’s paramount feature is its business line of credit. With this offering, businesses are allowed to serve only the amount drawn down from the loan balance, not the entire loan. As such, they’re spared the expenses of loans that sit idle while also enjoying seamless access to more funds as the need arises.

The platform’s line of credit comes in different forms and can be used for a variety of purposes, including:

- Commercial loans

- Short-term business loans

- Working capital

- Merchant cash loans

- Equipment loans

- Factory loans

- Industry-specific loans

How Do Kabbage Funding Loans Work?

To get a loan on the platform, you must have an active business checking account on Kabbage or American Express and an active card issued by American Express that’s at least 6 months old.

You might still qualify if you don’t have all of this, but the preapproval process might take a toll on your credit score.

Before applying, make sure to check whether their pre-approval will affect your credit score. Kabbage Funds will verify your business information using consumer and commercial reports obtained from various agencies, but their methods could have an impact on your score.

Also, you need a credit score of at least 640, an annual revenue of at least $50,000, and you must be in business for at least a year.

Once your details have been verified and you qualify, the rest is easy. Just sign on the dotted lines of the loan agreement, and your account will be credited, and your loan ready to draw down within days.

Loans are usually approved and posted to the loanee’s designated account within three business days of signing the loan agreement.

Loan Terms and Conditions

Here are some of the most notable terms in Kabbage Funds’ loans terms:

- Loan fees and loan term range:

- 2% – 9% for 6-month loans; 4.5% – 18% for 12-month loans; and 6.75% – 27% for 18-month loans.

- Outstanding balances and late payments may apply under certain circumstances.

- A personal guarantee for all loan

- Separate terms for both the full loan and the installment loan

- Monthly repayment schedules

Types of Businesses Best for Kabbage Loans

Fair-credit borrowers

Perhaps the group of borrowers who’ll appreciate Kabbage Funds the most is fair credit borrowers. Kabbage Funds’ minimum credit score requirement is 640, well below those of traditional lenders.

Business owners in need of flexible financing:

Kabbage loans offer flexibility in many areas. First, you can choose loan term lengths in multiples of 6-month terms, – 6 months, 12 months, or 18 months. You’re also allowed to take out more than one type of loan per time in your line of credit.

New businesses:

Startups and new ventures can assess quick, flexible, low-cost loans to cover their operational costs until they break even.

Borrowers in need of same-day loans:

Kabbage funds can come in handy anytime you need a quick loan, whether to clear a long-standing debt or to solve an urgent issue with your online business. From start to finish, you can apply for a loan and get it in just a couple of days.

How to Apply for a Loan on Kabbage

You can apply for Kabbage funding within just a few minutes. First, you need to check to see if you’re eligible for the type of loan you want and also if the preapproval process will have any impact on your credit score.

Once you have that sorted, follow these steps to apply for your loan:

1) Set up your account either through their website or mobile app. If you already have an American Express account, simply log in using your Amex credentials.

2) Fill out the form on the application window – you’ll need details like your business name and contact details, business tax ID, social security number, etc.

3) Wait for Kabbage to verify your information. If everything checks out well, your details could be verified within minutes.

4) If your application is approved, you’ll be sent a loan agreement. This will contain the final details like the loan amount, the repayment terms, and the loan duration.

Once you sign on this, your loan bank account will be credited within 3 business days.

To help you determine whether Kabbage is the best place to source your business loans and banking, let’s take a look at what some of its closest rivals have to offer.

Powerfully Simple Business Banking | Novo

Powerfully Simple Business Banking | Novo

Get a business edge with an award-winning, free business checking account from Novo.

Trusted by over 175,000 small businesses.

- No Hidden Fees, Minimum Balance

- Reserves for Expenses

- Mobile & Desktop Banking

- Customer Support is On App

- No Loan Options

1) Novo

Novo is an SMB banking platform that was founded in 2008 and acquired by American Express national bank in 2021. Although they now share the same parent company, Novo differs from Kabbage funding in many departments.

For starters, Novo isn’t just a direct lending platform. They are also an SBA loan platform, hosting a marketplace for third-party SMB lenders. That implies access to more financing options.

Most of their financing options are lines of credit with 6, 12, and 18-month repayment periods issued based on creditworthiness

Like Kabbage funding, Novo provides many important banking features for small businesses. They offer a business checking account with unique features like invoicing and accounting features.

They also support local and international transactions through wire transfers, ATM transfers, etc.

Their checking accounts are free of charges like minimum balance fees, monthly fees, overdraft fees, or transaction limits.

When it comes to services, Novo customers can manage their accounts via a mobile app. They can also sync data between their Novo app and many other business apps, from payment processors like PayPal and Wise to accounting software like Quickbooks.

Kabbage Vs Novo Head-to-Head Comparison

| Loan terms and conditions | Kabbage | Novo |

| Type of Financing | Line of credit | SBA loans, line of credit, equipment financing, merchant cash advance |

| Loan limits | $2000 – $100,000 | $1,000 to $500,000 |

| Interest rate | None | 7% – 25% |

| Minimum annual revenue | $50,000 | Depends on the lender |

| Repayment duration | Monthly | Varies based on lenders |

| Minimum credit score | 640 | 680 |

| Transaction fees | $25 fee for outgoing domestic wire transfer, No fees for out-of-network ATMs except for ATM operator fees | Depends on the third-party payment processor charges. Also, Novo reimburses any ATM fees at any location worldwide. |

| APY | 1.1% on balances of up to $100,000 | None |

Data source: Fundera

Our simple, accessible end-to-end banking solutions are tailor-made to

help small businesses thrive. Welcome to business banking done right.

- No Monthly Fees

- No Minimum Balance

- Business Checking w/Interest

- Cash Deposits Limited

- Deposit Service Fees

2) BlueVine

BlueVine gives Kabbage a good run for its money with slightly lower rates, faster loan disbursement (most loans are issued the same day), and a lower credit score requirement of 600 (sometimes as low as 500).

BlueVine also offers a fighting chance to much younger businesses.

Six-month-old businesses may be eligible for loans that range from $2,000 to $250,000.

Like Kabbage, BlueVine borrowers can draw down their loans whenever without worrying about extra fees like total monthly fees incurred, maintenance fees, origination fees, prepayment penalties, penalties for an outstanding balance, and other general fees.

BlueVine customers can also access an interest-bearing business checking account with reserve accounts for asset separation on the platform.

Besides the significantly higher borrowing limit, BlueVine also edges Kabbage in areas like annual percentage yield (APY) and a richer software ecosystem, making it more attractive to business owners.

Another area where BlueVine shines through is transparency. For one, you can hardly find anyone to talk to on Kabbage – customer care conversations begin and end with chatbots.

They’re also not clear on many critical issues like their minimum credit score requirement and other loan requirements.

BlueVine not only has responsive customer care that’s manned by humans, but they’re also very upfront – just about everything you’d need to know is already up on their website.

BlueVine Vs Kabbage: Head-to-Head Comparison

| Loan terms and conditions | Kabbage | BlueVine |

| Type of Financing | Line of credit | Line of credit |

| Minimum annual revenue | $50,000 | $120,000 |

| Opening deposit and minimum balance | None | None |

| APY | 2.0% on balances of up to $100,000 for eligible | 1.1% on balances of up to $100,000 |

| Teller cash withdrawal fees | None | $3 per transaction |

| Software integrations | Only payment integrations like PayPal and Stripe | Both payment integrations and accounting software like |

| Customer support | A dedicated team of professionals is available around the clock by phone and email | Mostly email |

Data source: Fit Small Business

Small Business Lending That's Fast and Easy

Small Business Lending That's Fast and Easy

OnDeck - America's Largest Online Small Business Lender. Term Loans up to $250K and Lines of Credit up to $100K. Get funds as soon as the same day.

- A+ BBB Rating

- Fast Funding

- Easy Application

- High-Interest Rates

- $100k Annual Revenue Requirement

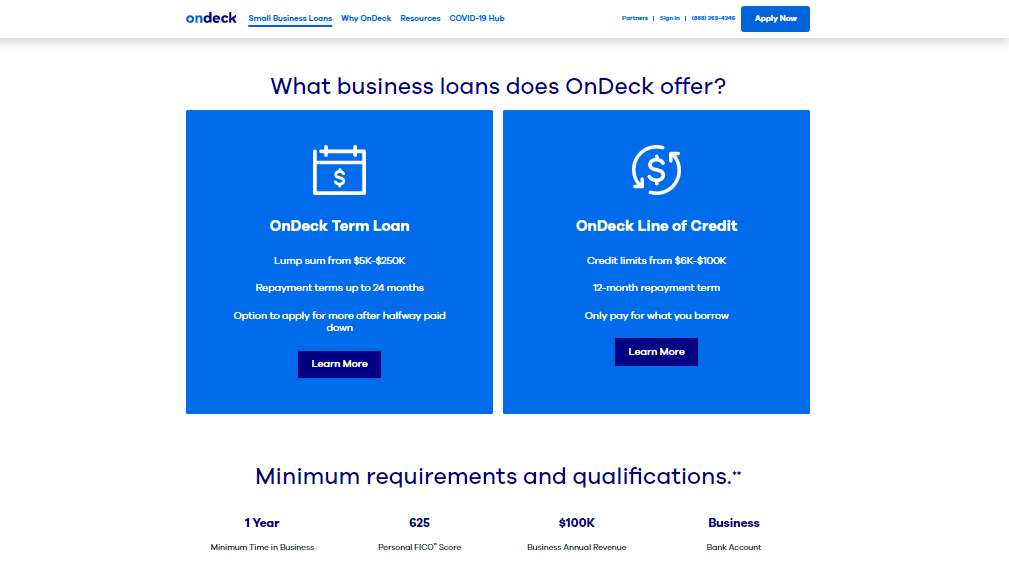

3) OnDeck

OnDeck Capital was founded in 2006 as a powerhouse for small business financing.

They have a much lower barrier to entry, with a much lower cut-off for credit score at 600, and fast approvals. In fact, most loans are posted on the same day of application.

They also offer many loan options, with multiple lines of credit ranging from $6000 up to $250,000.

One of the key advantages is their flexible terms.

For instance, with the $100,000 line of credit, borrowers can borrow up to $100,000 for 12 months, with the limit reset every time they draw on the line, so long as it’s below $100,000. That means you don’t have to wait another 12 months to regain your full borrowing limit.

The same goes for the second credit line, with a $250,000 limit and a repayment period of 18 months.

One major drawback, however, is that you must have at least $100,000 in incoming cash flow to qualify, which is double what Kabbage funding requires.

Your business must also be at least one year old.

OnDeck vs Kabbage: Head-to-Head Comparison

| Loan Terms and Conditions | Kabbage | OnDeck |

| Repayment schedule | Monthly | Daily or weekly |

| Collateral | None | Blanket Uniform Commercial Code (UCC) filing |

| Personal guarantee | Required | Required |

| Monthly advance fee | 6-month: 0.25% to 3.5%12-month: 0.25% to 2.75%18-month: 0.25% to 2.5% | None |

| Interest rate | None | 9% |

| Origination fee | None | Up to 5% |

| Estimated APR | 3% – 42% | 35% – 100% |

| Annual revenue | $50,000 | $100,000 |

Data source: Fit Small Business

FAQs

Does Kabbage offer a good checking account?

Kabbage funding offers a handy checking account that’s accessible through an intuitive mobile interface. Their checking account comes with enticing features like zero monthly fees, no fees for ACH and international wires, plus support for an unlimited number of transactions and a competitive APY of 1.1%.

Do Kabbage loans require collateral?

The only form of guarantee that Kabbage requires is a personal guarantee from the business owner to pay back the loan. There’s no need for any personal collateral or business collateral, and this significantly eases and speeds up the loan approval process.

What is the minimum credit score required by SBA?

SBA loans are directly geared toward small businesses, and SBA uses FICO Small Business Scoring Service (SBSS) rather than a personal credit score to check the financial health of borrowers.

This is a different score based on the business owner’s credit bureau score as well as other financials. It ranges from 0 to 300, and businesses must score at least 155 to qualify for an SBA loan.

Where do online lending platforms operate?

Platforms like Kabbage Funding, BlueVine, and Novo are available across all 50 states and all U.S. territories. OnDeck is available in all states except Nevada, North Dakota, and South Dakota.

Final Thoughts: No Shortfall of Quick Funding Options for your Small Business

As a business owner, extra funds can always come in handy now and then, whether you’re experiencing payment delays from customers, struggling with cash flow problems due to off-seasons, or looking to expand to other locations.

With Kabbage and the other top-notch loaning platforms in this guide, you’re always a heartbeat away from securing the extra cash you need to move forward with your business.

The lenders in this review share quite a lot in common – a fast application process, low rates, and flexible terms. But the slight differences between their offers can mean a lot for your business, so do your due diligence when considering your options.

Once you’re settled on an option, you can start out with a smaller loan to see how the process works. If it’s favorable enough, you can then go in for more.

Now, there’s one less excuse to get the funding your business needs today!

![Asana vs Monday: Ultimate Guide [2023]](https://alexmedawar.com/wp-content/uploads/2023/01/The-sales-CRM-software-thats-fully-customizable-monday-com.jpg)

![NetSuite vs QuickBooks: The Ultimate Comparison Guide [2023]](https://alexmedawar.com/wp-content/uploads/2022/05/Accounting-Software-for-Small-Business-QuickBooks®.png)